This year’s Bitcoin rally has caught many smart people by surprise.

In “Shuggie Bain,” Douglas Stuart’s award-winning and harrowing depiction of alcoholism, sectarianism and deprivation in post-industrial Scotland, money is always scarce and often dirty. Deserted by her second husband and unable to hold down a job, Shuggie’s mother, Agnes, relies on her twice-a-week child benefit to feed her children — or her booze habit. As the latter nearly always wins, she and Shuggie are regularly reduced to desperate expedients to fend off starvation: Extracting coins from electricity and television meters, pawning their few valuable possessions, and ultimately selling their bodies for brutal sexual favors.

Stuart vividly captures the miseries of a Glasgow of greasy coins and filthy banknotes. After one of many wretched copulations in the back of a taxi, one of Agnes’s lovers inadvertently showers her with coins from his pocket. Shuggie’s father briefly reappears at one point, handing his son two 20-pence pieces from his taxi’s change dispenser by way of a gift, grudgingly adding four 50-pence pieces when the boy looks nonplused. (“Don’t ask for mair!”) The “rag-and-bone man,” who goes from house to house buying old clothes and junk, pays “with a roll of grubby pound notes” bound by an old Band-Aid. The image is especially startling because banknotes have so rarely featured in the narrative. The only credit in this world is from rent-to-own catalogues, the Provident doorstep lender, and a few hard-pressed shopkeepers.

I grew up in middle-class, mostly sober Glasgow, but I still remember the tyranny of those damned coins: the nightmare of having too few for a bus fare or the wrong sort for a phone box. To my children, all this is as much a part of ancient lore as pirate chests of doubloons once were to me. Coins are fast fading from their lives, soon to be followed by banknotes. In some parts of the world — not only China but also Sweden — nearly all payments are now electronic. In the US, debit card transactions have exceeded cash transactions since 2017. Even in Latin America and parts of Africa, cash is yielding to cards and a growing number of people manage their money through their phones.

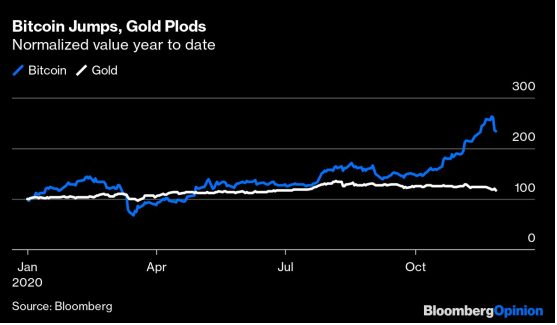

We are living through a monetary revolution so multifaceted that few of us comprehend its full extent. The technological transformation of the internet is driving this revolution. The pandemic of 2020 has accelerated it. To illustrate the extent of our confusion, consider the divergent performance of three forms of money this year: the US dollar, gold and Bitcoin.

The dollar is the world’s favorite money, not only dominant in central bank reserves but in international transactions. It is a fiat currency, its supply determined by the Federal Reserve and US banks. We can compute its value relative to the goods consumers buy, according to which measure it has scarcely depreciated this year (inflation is running at 1.2%), or relative to other fiat currencies. On the latter basis, according to Bloomberg’s dollar spot index, it is down 4% since Jan. 1. Gold, by contrast, is up 15% in dollar terms. But the dollar price of a bitcoin has risen 139% year-to-date.

This year’s Bitcoin rally has caught many smart people by surprise. Last week’s high was just below the peak of the last rally ($19,892 according to the exchange Coinbase) in December 2017. When Bitcoin subsequently sold off, the New York University economist Nouriel Roubini didn’t hold back. Bitcoin, he told CNBC in February 2018, had been the “biggest bubble in human history.” Its price would now “crash to zero.” Eight months later, Roubini returned to the fray in congressional testimony, denouncing Bitcoin as the “mother of all scams.” In tweets, he referred to it as “Shitcoin.”

Fast forward to November 2020, and Roubini has been forced to change his tune. Bitcoin, he conceded in an interview with Yahoo Finance, was “maybe a partial store of value, because … it cannot be so easily debased because there is at least an algorithm that decides how much the supply of bitcoin raises over time.” If I were as fond of hyperbole as he is, I would call this the biggest conversion since St. Paul.

Roubini is not the only one who has been forced to reassess Bitcoin this year. Among the big-name investors who have turned bullish are Paul Tudor Jones, Stan Druckenmiller and Bill Miller. Even Ray Dalio admitted the other day that he “might be missing something” about Bitcoin.

Financial journalists, too, are capitulating: On Tuesday, the Financial Times’s Izabella Kaminska, a long-time cryptocurrency skeptic, conceded that Bitcoin had a valid use-case as a hedge against a dystopian future “in which the world slips towards authoritarianism and civil liberties cannot be taken for granted.” She is on to something there, as we shall see.

So what is going on?

First, we should not be surprised that a pandemic has quickened the pace of monetary evolution. In the wake of the Black Death, as the historian Mark Bailey noted in his masterful 2019 Oxford Ford lectures, there was an increased monetisation of the English economy. Prior to the ravages of bubonic plague, the feudal system had bound peasants to the land and required them to pay rent in kind, handing over a share of all produce to their lord. With chronic labor shortages came a shift toward fixed, yearly tenant rents paid in cash. In Italy, too, the economy after the 1340s became more monetised: It was no accident that the most powerful Italian family of the 15th and 16th centuries were the Medici, who made their fortune as Florentine moneychangers.

In a similar way, Covid-19 has been good for Bitcoin and for cryptocurrency generally. First, the pandemic accelerated our advance into a more digital word: What might have taken 10 years has been achieved in 10 months. People who had never before risked an online transaction were forced to try, for the simple reason that banks were closed. Second, and as a result, the pandemic significantly increased our exposure to financial surveillance as well as financial fraud. Both these trends have been good for Bitcoin.

I never subscribed to the thesis that Bitcoin would go to zero after it plunged in price in late 2017 and 2018. In the updated 2018 edition of my book, “The Ascent of Money” — the first edition of which appeared more or less simultaneously with the foundational Bitcoin paper by the pseudonymous Satoshi Nakamoto — I argued that Bitcoin had established itself as “a new store of value and investment asset — a type of ‘digital gold’ that provides investors with guaranteed scarcity and high mobility, as well as low correlation with other asset classes.”

“Satoshi’s goal,” I argued, “was not to create a new money but rather to create the ultimate safe asset, capable of protecting wealth from confiscation in jurisdictions with poor investor protection as well as from the near-universal scourge of currency depreciation … Bitcoin is portable, liquid, anonymous and scarce … A simple thought experiment would imply that $6,000 is therefore a cheap price for this new store of value.”

Two years ago, I estimated that around 17 million bitcoins had been mined. The number of millionaires in the world, according to Credit Suisse, was then 36 million, with total wealth of $128.7 trillion. “If millionaires collectively decided to hold just 1% of their wealth as Bitcoin,” I argued, “the price would be above $75,000 — higher, if adjustment is made for all the bitcoins that have been lost or hoarded. Even if the millionaires held just 0.2% of their assets as Bitcoin, the price would be around $15,000.” We passed $15,000 on November 8.

What is happening is that Bitcoin is gradually being adopted not so much as means of payment but as a store of value. Not only high-net-worth individuals but also tech companies are investing. In July, Michael Saylor, the billionaire founder of MicroStrategy, directed his company to hold part of its cash reserves in alternative assets. By September, MicroStrategy’s corporate treasury had purchased bitcoins worth $425 million. Square, the San Francisco-based payments company, bought bitcoins worth $50 million last month. PayPal just announced that American users can buy, hold and sell bitcoins in their PayPal wallets.

This process of adoption has much further to run. In the words of Wences Casares, the Argentine-born tech investor who is one of Bitcoin’s most ardent advocates, “After 10 years of working well without interruption, with close to 100 million holders, adding more than 1 million new holders per month and moving more than $1 billion per day worldwide,” it has a 50% chance of hitting a price of $1 million per bitcoin in five to seven years’ time.

Whoever he is or was, Satoshi summed up how Bitcoin works: It is “a purely peer-to-peer version of electronic cash” that allows “online payments to be sent directly from one party to another without going through a financial institution.” In essence, Bitcoin is a public ledger shared by a network of computers. To pay with bitcoins, you send a signed message transferring ownership to a receiver’s public key. Transactions are grouped together and added to the ledger in blocks, and every node in the network has an entire copy of this blockchain at all times. A node can add a block to the chain (and receive a bitcoin reward) only by solving a cryptographic puzzle chosen by the Bitcoin protocol, which consumes processing power.

Nodes that have solved the cryptographic puzzle — “miners,” in Bitspeak — are rewarded not only with transaction fees (5 bitcoins per day, on average), but also with additional bitcoins — 900 new bitcoins per day. This reward will get cut in half every four years until the total number of bitcoins reaches 21 million, after which no new bitcoins will be created.

There are three obvious defects to Bitcoin. As a means of payment, it is slow. The Bitcoin blockchain can process only around 3,000 transactions every 10 minutes. Transaction costs are not trivial: Coinbase will charge a 1.49% commission if you want to buy one bitcoin.

There is also a significant negative externality: Bitcoin’s “proof-of-work” consensus algorithm requires specialised computer chips that consume a great deal of energy — 60 terawatt-hours of electricity a year, just under half the annual electricity consumption of Argentina. Aside from the environmental costs, one unforeseen consequence has been the increasing concentration of Bitcoin mining in a relatively few hands — many of them Chinese — wherever there is cheap energy.

But these disadvantages are outweighed by two unique features. First, as we have seen, Bitcoin offers built-in scarcity in a virtual world characterised by boundless abundance. Second, Bitcoin is sovereign. In the words of Casares, “No one can change a transaction in the Bitcoin blockchain and no one can keep the Bitcoin blockchain from accepting new transactions.” Bitcoin users can pay without going through intermediaries such as banks. They can transact without needing governments to enforce settlement.

The advantages of scarcity are obvious at a time when the supply of fiat money is exploding. Take M2, a measure of money that includes cash, bank accounts (including savings deposits) and money market mutual funds. Since May, US M2 has been growing at a year-on-year rate above 20%, compared with an average of 5.9% since 1982. The future weakness of the dollar has been a favorite 2020 talking point for Wall Street economists such as Steve Roach. You can see why. There really are a lot of dollars around, even if their velocity of circulation has slumped because of the pandemic.

The advantages of sovereignty are less obvious but may be more important. Bitcoin is not the only form of digital money that has flourished in 2020. China has been advancing rapidly in two different ways.

Nowhere in the world are mobile payments happening on as large a scale as in China, thanks to the spectacular growth of Alipay and WeChat Pay. Those electronic payment platforms now handle close to $40 trillion of transactions a year, more than double the volume of Visa and Mastercard combined, according to calculations by Ribbit Capital. The Chinese platforms are expanding rapidly abroad, partly through investments in local fintech companies by Ant Group and Tencent.

At the same time, the People’s Bank of China has accelerated the rollout of its digital currency. The potential for a digital yuan to be adopted for remittance payments or cross-border trade settlements is substantial, especially if — as seems likely — countries participating in the One Belt One Road program are encouraged to use it. Even governments that are resisting Chinese financial penetration, such as India, are essentially building their own versions of China’s electronic payments systems.

Some economists, such as my friend Ken Rogoff, welcome the demise of cash because it will make the management of monetary policy easier and organised crime harder. But it will be a fundamentally different world when all our payments are recorded, centrally stored, and scrutinised by artificial intelligence — regardless of whether it is Amazon’s Jeff Bezos or China’s Xi Jinping who can access our data.

In its early years, Bitcoin suffered reputational damage because it was adopted by criminals and used for illicit transactions. Such nefarious activity has not gone away, as a recent Justice Department report makes clear. Increasingly, however, Bitcoin has an appeal to respectable individuals and institutions who would like at least some part of their economic lives to be sheltered from the gaze of Big Brother.

It is not (as the term “cryptocurrency” misleadingly implies) that Bitcoin is beyond the reach of the law or the taxman. When the Federal Bureau of Investigation busted the online illegal goods market Silk Road in 2013, it showed how readily government agencies can trace the counterparties in suspect Bitcoin transactions. This is precisely because the blockchain is an indelible record of all Bitcoin transactions, complete with senders’ and receivers’ bitcoin addresses.

Moreover, the Internal Revenue Service is perfectly prepared to demand information on bitcoin accounts from exchanges, as Coinbase discovered in 2016. A rumor of new US Treasury regulations requiring greater disclosures by exchanges caused a sharp crypto selloff over Thanksgiving. The point is simply that the financial data of law-abiding individuals is better protected by Bitcoin than by Alipay. As the Stanford political theorist Stephen Krasner pointed out more than 20 years ago, sovereignty is a relative concept.

Rather than seeking to create a Chinese-style digital dollar, Joe Biden’s nascent administration should recognise the benefits of integrating Bitcoin into the US financial system — which, after all, was originally designed to be less centralised and more respectful of individual privacy than the systems of less-free societies.

Life in the East End of Glasgow in the 1980s was nasty, brutish and short of money. But all those transactions in grubby pounds and pence — genuine shitcoins — were, if nothing else, private. If Agnes Bain bought Special Brew instead of oven chips, it was a matter for her, the shopkeeper, and her long-suffering kids; the state was none the wiser. That was scant consolation to poor Shuggie. But, as we have learned again this year, a free society comes at a price that is not always payable in cash.

Read the full article HERE